CPA FAQ's

Corporate Structures and Tax Rates

C Corporations

For federal income tax purposes, a C corporation is recognized as a separate taxpaying entity. C corporations conduct business, realize net income or losses, pay taxes, and distribute profits to shareholders. C corporation profits are taxed to the corporation when earned, and then taxed to the shareholders when distributed as dividends. This creates a double tax. In select circumstances, however, net income will be higher, even after the double tax, than it would be for sole proprietors or individuals in the top tax brackets. This in mind, it is important to plan ahead by estimating personal income, business income, and dividends, and evaluating the corresponding tax rates.

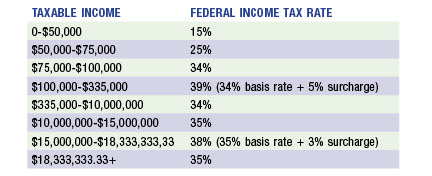

This table specifies the Federal income tax rate schedule for C corporations, current through 2014.

Personal Holding Company

In addition to C corporation graduated taxes, personal holding companies pay a flat 15% on all undistributed income. Personal holding company status is determined by a two part income and stock ownership test.

Income Test. At least 60% of its adjusted ordinary gross income for the taxable year is passive income, e.g. interest, dividends, rents, royalties.

Stock Ownership Test. More than 50% of the stock value is owned by 5 or fewer individuals.

This tax can be avoided by structuring your business as an S corporation.

S Corporation

can avoid double taxation by incorporating as an S corporation. Corporate income passes-through to individual shareholders, who file their share of corporate gains, losses, deductions and credits on their personal tax returns. While the prospect of bypassing C corporation double taxation is enticing, it is important to estimate future income and weigh the corresponding tax rates. Each business scenario is unique, and warrants a thorough evaluation to get at the business structure that most decreases taxes, limits liability, and maximizes profits.

Qualified Personal Service Corporations

Some corporations, like qualified personal service corporations, cannot alter their corporate structure to take advantage of lower tax rates. Whereas other C corporations have the benefit of a tax schedule keyed to income, and S corporations have the benefit of a pass-through to shareholders, qualified personal service corporations pay a flat 35% rate on all taxable income.

Qualified personal service corporation status is determined by a two part test looking at business function and ownership.

Function Test. 95% of all business activities involve performance of services in the fields of health, law, engineering, architecture, accounting, actuarial science, performing arts, or consulting.·

Ownership Test. Substantially all of the stock must be owned by current and retired employees.

If a corporation meets the above function and ownership test, it must pay a federal tax rate of 35 percent on its income, starting with dollar one. Hence, it is important to assess your business against the definition of a qualified personal service corporation. If you fit the personal service criteria, plan ahead by distributing all corporate revenue as salaries, bonuses, and expenses, with a final corporate income of zero.

COPYRIGHT 2016 DONNA L. RODRIGUEZ PLLC